Should We Blame Joe Biden?

June 13, 2022

Stock Prices, Inflation, Recession & Economic Cycles

Economic cycles – also known as business cycles — are a reality, and they can be tracked over time. They generally are predictable, although not in precise time frames. Economic cycles consist of four identifiable phases or stages: (a) Expansion; (b) Peak; (c) Contraction; and (d) Trough.

Every economic cycle includes a period of euphoria and exuberance marked by a sustained period of economic growth; followed by a period of uncertainty and lethargy linked to a period of economic decline.

When Donald Trump took office in January 2017, he inherited an economy in its 91st month of economic expansion following the end of the Great Recession in June 2009. That expansion continued into 2020, becoming the longest period of expansion on record, peaking at 128 months in February 2020.

We know that Donald Trump never fails to speak his mind. During the campaign leading to the 2020 presidential election, Trump proclaimed, “If (Joe Biden) is elected, the stock market will crash!”

[In 2018, Trump said, “When a country (USA) is losing many billions of dollars on trade with virtually every country it does business with, trade wars are good, and easy to win.” In late January 2020, Trump also said, “We have it (coronavirus) totally under control. It’s one person coming in from China. It’s going to be just fine.”]

Facts are facts:

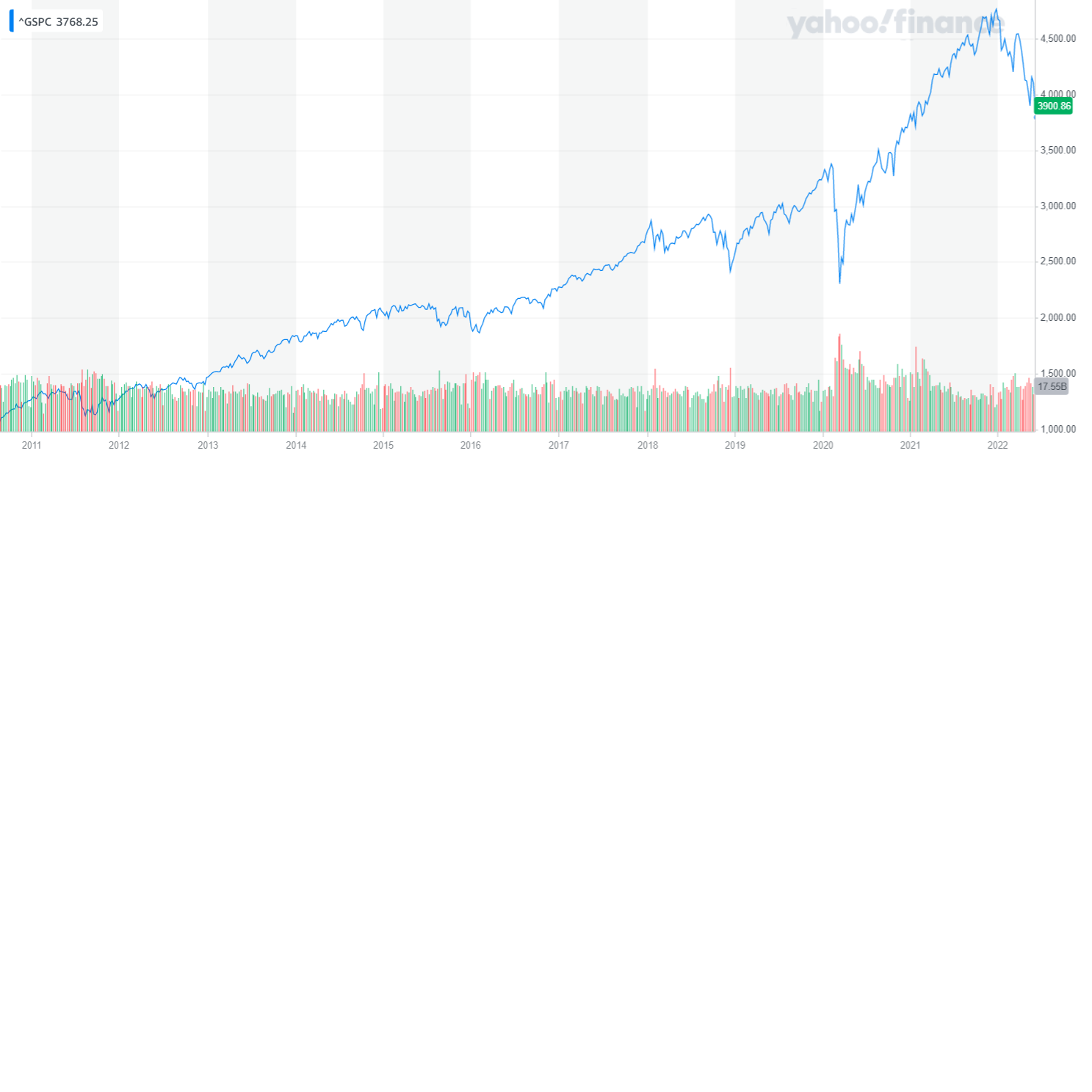

- The S&P 500 fell from 4,766 in late December 2021 to 3,900 today, a 20% loss;

- We’ve seen the price of gasoline hit $5.00 per gallon, up from $3.00 just a year ago;

- Case-Shiller recently reported a 34.8% price increase for housing in the Tampa Bay area (where I currently live) from March 2021 to March 2022;

- The most recent CPI report reflects an annual rate of 8.6 percent through May 2022, the fastest rate in four decades.

What’s really going on?

There are a number of pieces to this puzzle, including:

- The lingering effects of a Pandemic;

- The Russian invasion of Ukraine;

- Aftershocks (direct and indirect) from draconian tariffs enacted beginning in 2018;

- Ongoing ripple effects from the 2017 Tax Cuts and Jobs Act (TCJA); and

- Various supply chain issues, both domestic and international.

But, the root cause of our current intersection of inflation and stock market volatility likely traces back to 2010, when the Fed launched “QE2” – quantitative easing – essentially increasing liquidity in the domestic economy to stimulate economic growth. One of the outcomes from QE is a decrease in bond prices due to falling interest rates, combined with a run-up in stock prices as investors search for yield.

When the Fed announced its QE2 plan in November 2010, 30 year mortgages were at 5%; and the S&P 500 index was 1,200. Over the course of the next few years, rates on 30 year mortgages dropped as low as 3.3%, and the S&P 500 index toward 2,010 (which it reached in September 2014).

Meanwhile, the CPI from 2010 to the end of 2020 remained relatively calm, reflecting the lagging effects of the economic recovery which began in mid-2009.

It is relatively easy to look into the rearview mirror now to observe that the Fed’s response to the impact of Covid on our economy helped to create an environment which fueled the inflation we are facing today. In March 2020, in addition to a promise to inject a $ Trillion into the U.S. banking system, the Fed cut the federal funds rate to a range of 0% to 0.25%.

Those actions of the Fed likely saved our economy from implosion, but also helped to inspire a dramatic run-up in stock prices: The S & P 500 index rose from 3,000 in early March 2020 to reach 4,700 in November 2021. (Stock prices were further affected by massive stock buybacks enabled by the 2017 TCJA).

While it seems convenient for some to blame Joe Biden for high gasoline prices; rapidly rising consumer prices; the stock market ‘meltdown’ — even for supply chain dysfunctions – history tells us there is a rather significant lag between the point when policy actions take place, until begin to see the results from those actions.

The Biden White House has pledged to fight against inflation and has stubbornly refused to blame the Fed for our current economic symptoms.

Although there are plenty of contributing factors, the real truth is over a decade of relying almost entirely on monetary policy to steer the ship brought us to this moment, not 18 months of Democratic control in the White House.