It is perfectly clear: no person is better suited than Ron DeSantis to challenge and conquer the hidden changes facing our nation, and no person will be a better steward of America in the years to come. Evil forces across our planet demand a great leader—someone strong but thoughtful; principled but inquisitive; and resolute in their belief in America’s noble mission.

DeSantis has proved to be an intrepid conservative in Florida. Under his leadership, Florida is bigger and more prosperous now than it was when he took office. There are more jobs; more people; more businesses; more morality; and less abortion; less grooming; and less tolerance for woke and CRT.

His leadership during the pandemic allowed Florida to thrive by keeping businesses open and kids in school, his economic policies have lowered taxes and brought prosperity and new business to Florida, and his unwavering commitment to standing up to woke ideology infiltrating our corporations and schools have distinguished Governor DeSantis as the one true leader American wants and needs, a man who never backs down from the needed fights to make our country better.

Florida has become the fastest growing state in the nation. But it’s not just that. It ranks #1 in education, and it’s because there is zero tolerance for ideologies which challenge White Christian morality, the very foundation of the U.S. Constitution.

Ron DeSantis has shown over and over again that he will protect and stand up for our children and grandchildren, young folks who are being hyper-sexualized at extremely young ages and maliciously influenced by radical activists. Donald Trump might provide lip service, but at the end of the day, he runs away from these challenges—or even joins the other side, whether it’s Disney’ Pfizer or Budweiser.

DeSantis will continue to fight for our values; our country; our children; our families; and for a bright future where America regains its position of righteous supremacy over the insidious forces of evil.

Make no mistake: Trump put on a good facade. He looked like a strong man, but he was unfocused and weak. He set the table for America’s enemies across the world to become more entrenched, allowing them to take Americans prisoner with no consequence. They’ve floated spy balloons over our airspace. They’ve launched full-scale invasions of other countries and toppled the democratic governments we spent decades building. All the while, America become more and more weak and complacent.

Governor DeSantis has proven himself to be the fighter America needs—from serving our country to taking on dangerous woke agendas. Trump might back down from battles against Disney, Pfizer and Budweiser, but not Ron DeSantis, and that is the big message for Republican primary voters.

Federal Debt Ceiling Observations

May 11, 2023

Hanging their hats on false equivalence

The underlying logic Speaker Kevin McCarthy and his crew lean on in their arguments relative to the federal debt ceiling rely on false equivalencies.

The gist of their message seems to be, “Just as families and businesses balance their checkbooks every month, we believe the federal government needs to make balancing the nation’s checkbook a top priority. Raising the debt ceiling is a short-term solution to a long- term problem. Before we consider raising the debt ceiling, our federal government needs to focus on reducing spending and living within its means to ensure a healthy economy for future generations”.

Sounds pretty good, right?

Yet, that explanation illuminates one of the greatest obstacles we face as a nation: A void of economic and financial understanding among most American adults.

The ‘checkbook’ is the equivalent of an annual budget. Current revenues flow in, and current expenses flow out. If revenues exceed expenses, there is a surplus. When revenues exactly equal expenses, it is ‘break even’. When expenses exceed revenues, there is a current-year deficit.

Staying with the household theme, the federal debt is most equivalent to a home mortgage, and the balance due is an accumulation of debt over time. Remember that new roof? That new kitchen? That fabulous backyard pool? Those were capital expenses, incurred in one year, but with an expected useful life of 10, 15, even 30 years. You add these expenses to the mortgage so that they get paid off over time.

As a retired professional in the field of finance and economics, when I hear Speaker McCarthy or members of his crew attempting to equate current spending to our overall aggregate debt obligations, I cringe.

Some rather simple adjustments to our tax code, including elimination of the carried interest loophole and raising the top corporate rate from 21% to 28% would make huge revenue contributions to balancing the annual (current FY) federal budget.

And, why is it that low- and moderate-income wage earners are required to make contributions to Social Security on every dollar of their earnings up to the current wage cap [a.k.a. ‘the contribution and benefit base’] of $160,200, yet those who are blessed to earn in excess of that amount are exempt from contributions to Social Security on earnings above that amount?

The wage cap on Medicare contributions was eliminated in the 1990’s, so even higher-income wage earners are required to make the 1.45% contribution to the Medicare tax with no limit on earnings.

We clearly have a revenue gap. Why does the cap on social security earnings continue to this day? And, those who claim their income not as ‘wages’ but as ‘carried interest’ not only receive beneficial income tax treatment, they also are exempt from FICA contributions. What a racket!

Federally guaranteed obligations are debt securities issued by the U.S. government, currently considered risk-free because they are backed by the full faith and credit of the federal government. When the Treasury sells these securities, they help to finance the federal debt outstanding at that time.

Allowing the government to default as an outcome from a false debate linking current revenues and spending to our long-term debt obligations would be a preventable tragedy of immense proportions.

Minority Leader Hakeem Jeffries (if you are listening): I implore you to be bold and to tear apart Speaker McCarthy’s logic map, and to take this opportunity to focus in on one of the greatest obstacles we face as a nation: A void of economic and financial understanding among most American adults. Until the American people awake from their deprivation of economic and financial principles, they will continue to be vulnerable to Alternative Facts such as those presented by Speaker McCarthy and his crew.

The Big Lebowski must have learned of McCarthy’s foolish and destructive crusade to equate and combine the federal debt ceiling with the current (2024) federal budget when he so eloquently said, “This will not stand, you know. This aggression will not stand, man”.

State of the Union 2023

February 8, 2023

Joe Biden & State of the Union

February 7, 2023 was the date when Joe Biden, our current POTUS, Number 46, stood at the podium in the U.S. Capitol to report on the State of the Union.

An executive summary of his remarks: “Because the soul of this nation is strong, because the backbone of this nation is strong, because the people of this nation are strong, the State of the Union is strong.”

It reminded me a bit of something I recall from an American History course many years ago, a speech by an elected official in the mid-19th century where it was said, “United We Stand, Divided We Fall”. A quick look back on that concept brought me to ancient Greece, and then to the Bible (Mark 3:25) as “And if a house be divided against itself, that house cannot stand.“

The Seal of the Commonwealth of Kentucky includes the phrase “United We Stand, Divided We Fall.”

There were plenty of elected officials seated in the U.S. Capitol to observe Mr. Biden’s State of the Union address. Most were dressed well; on good behavior; and showing respect for the congressional rules of decorum. A few of the elected officials seated in the Capitol were unable to control their emotions, and some of those exhibited bad – Really Bad — behavior.

Sad. Very Sad…

One takeaway from this major event is that Mr. Biden didn’t: (1) vote for or against the Tax Cuts and Jobs Act of 2017 (possibly the worst legislation of the 21st century to date); (2) dissolve the White House Pandemic Response Team; (3) say, “The CDC and my Administration are doing a GREAT job of handling Coronavirus!”; (4) set the stage for a mass genocide of the American people; (5) bring the entire US economy to its knees; (6) create tariffs on thousands of products which resulted in the imposition of some $80 Billion of the equivalent of new taxes on American consumers, one of the largest tax increases in decades, setting a solid foundation for record price inflation once the US economy began to recover; (7) create a new addition to the already bloated Pentagon — the U.S. Space Force — adding about $20+ Billion to an obscene defense budget; or (8) enable the passage of legislation to raise the U.S. debt ceiling from $19.6 Trillion (end of 2016) to $27.8 Trillion (end of 2020).

Despite his inability to claim ownership of the above accomplishments, it seems that Biden has accomplished a great deal of positive actions on his own in just 2 years, with very little fanfare.

It also seems that Mr. Biden constantly is in the gunsights of a well-oiled opposition team, very well-funded by Dark Money.

What puzzles me: What is the endgame for these Dark Money folks?

Is it a return to Feudalism? Or maybe, replication of the Putin model of controlled oligarchy? If that, then will Putin control the final model, or will it be someone else?

The virtual elimination of a reliable, well-supported and highly ethical Fourth Estate in the U.S. has been a major strategic victory by the Dark Money folks in this apparent war against successful continuation of the great American Experiment.

Just curious (and asking for a friend): Is that Biden’s fault, too?

I Don’t Love Joe Biden

October 20, 2022

But should we blame him for our current economic malaise?

When I was a young pup, I remember Uncle Cal frequently referring to certain elected officials as “a Horse’s Ass”. Back then, I didn’t know what he was trying to infer, but it sure sounded good!

Uncle Cal is long gone, but it seems the supply of Horse’s Ass elected officials has expanded significantly and I’m frustrated, angry and simply miserable as I watch and listen to ‘broadcast journalists’ and various political pundits who seem to have no grasp of economics as they explain current economic conditions to an audience of [potentially] economic illiterates. Thus, the origin of my current ‘rant’:

Stock Prices, Inflation, Recession & Economic Cycles

Economic cycles – also known as business cycles — are a reality, and they can be tracked over time.

They generally are predictable, although not in precise time frames. Economic cycles consist of four identifiable phases or stages: (a) Expansion; (b) Peak; (c) Contraction; and (d) Trough.

Every economic cycle includes a period of euphoria and exuberance marked by a sustained period of economic growth; followed by a period of uncertainty and lethargy linked to a period of economic decline.

The Great Recession officially ended in June 2009. By the time Donald Trump took office in January 2017, he inherited an economy in its 91st month of economic expansion.

That expansion continued into 2020, becoming the longest period of expansion on record, peaking at 128 months in February 2020.

Donald Trump has never failed to speak his mind. During the campaign leading to the 2020 presidential election, Trump proclaimed, “If (Joe Biden) is elected, the stock market will crash!”. [In 2018, Trump said, “When a country (USA) is losing many billions of dollars on trade with virtually every country it does business with, trade wars are good, and easy to win.” In late January 2020, Trump also said, “We have it (coronavirus) totally under control. It’s one person coming in from China. It’s going to be just fine.”]

Facts are facts:

- Five years ago (October 20, 2017) the S&P 500 closed at 2,575; it closed today (10/20/2022) at 3,666, an overall 5 year gain of 42%; an average of 7.3% per year.

- Ten years ago (October 2012), gasoline sold for $3.62 per gallon in Florida. AAA shows the current Florida price per gallon at $3.38.

- Case-Shiller reported a ten year 288% price increase for housing in the Tampa Bay area (where I currently live) from Mid-2012 to Mid-2022. This is partly due to (1) recovery from the Great Recession; (2) stimulus due to artificial below market interest rates (Fed Policy); and (3) supply/demand imbalance primarily due to local and regional housing policy decisions over time.

- The most recent CPI-U release from BLS reflects an annual inflation rate of 8.2 % through September 2022, the highest in four decades. Yet, if we look back to 2012, we can see the average annual rate over that decade computes to about 2.5% annually, with near zero periods during the Pandemic.

What’s really going on? There are a number of pieces to this puzzle, including:

- The lingering effects of a Pandemic;

- The Russian invasion of Ukraine;

- Aftershocks (direct and indirect) from draconian tariffs enacted beginning in 2018;

- Ongoing ripple effects from the 2017 Tax Cuts and Jobs Act (TCJA); and

- Various supply chain issues, both domestic and international.

The root cause of our current intersection of inflation and stock market volatility likely traces back to 2010, when the Fed launched “QE2” – quantitative easing – essentially increasing liquidity in the domestic economy to stimulate economic growth. One of the outcomes from QE is a decrease in bond prices due to falling interest rates, combined with a run-up in stock prices as investors search for yield.

When the Fed announced its QE2 plan in November 2010, 30-year mortgages were at 5%; and the S&P 500 index was 1,200. Over the course of the next few years, rates on 30-year mortgages dropped as low as 3.3%, while the S&P 500 index inched toward 2,010 (which it reached in September 2014).

Meanwhile, the CPI from 2010 to the end of 2020 remained relatively calm, reflecting the lagging effects of the economic recovery which began in mid-2009.

It is relatively easy to look into the rearview mirror now to observe that the Fed’s responses to (a) the Great Recession; and then (b) impacts of Covid on our economy helped to create an environment which fueled the inflation we are facing today.

In March 2020 — in addition to a promise to inject a Trillion dollars into the U.S. banking system — the Fed cut the federal funds rate to a range of 0% to 0.25%.

The rapid and aggressive response by the Fed likely saved our economy from implosion, but also helped inspire a dramatic run-up in both stock prices and home prices: The S & P 500 index rose from 3,000 in early March 2020 to reach 4,700 in November 2021 as investors chased phantom returns on investment. (Stock prices were further bolstered by massive stock buybacks inspired by the 2017 TCJA).

Home mortgage interest rates are a critical determinant of purchasing power for most borrowers. As far back as 1971, 30 year fixed-rate mortgages had never been offered below 7%; they moved up to 9% in 1974; climbed to 11% in 1979; and reached a peak of 16.6% in 1981.

Our economy is a long game. The few months when home mortgage interest rates were at or below 5% is an aberration enabled by Fed policy. Now that long-term mortgage rates have settled into the 7% to 9% range [which seems rationale and appropriate based on history], home prices will also stabilize.

It seems convenient for some to blame Joe Biden for (a) high gasoline prices; (b) rapidly rising consumer prices; (c) a stock market ‘meltdown’; and (d) even for supply chain dysfunctions.

A quick look at history confirms that there is a rather significant lag between the point when policy is affirmed and enacted; and the future point when we begin to see and experience results from those actions.

The Biden White House has pledged to fight against inflation, and has stubbornly refused to blame the Fed for our current economic symptoms.

Although there seem to be plenty of contributing factors, the real truth is: We relied almost entirely on monetary policy to steer the ship for more than a decade, and that approach brought us to this moment, not 24 months of Democratic control in the White House.

And, if the Fed would just slow down their relentless and uncompromising initiatives to raise interest rates to the point of choking off the economy as they attempt to rein in inflation, we might experience a smooth correction, and a gentle return to the economic expansion phase we all want to see.

Financial Literacy & Student Loans

September 6, 2022

Dear Senator Cotton:

One of the most recent national events which amplified the chasm between political party affiliations in the U.S. was the August 24, 2022 announcement by President Biden of a plan to wipe out significant amounts of student loan debt for tens of millions of low- and moderate-income Americans.

Sen. Tom Cotton (R, Ark) was on the rapid response team to counter the Biden announcement, saying:

“There is no such thing as student loan forgiveness—this is a bailout, paid for by the large majority of Americans who never went to college or who responsibly paid off their debts. President Biden’s plan ignores the true culprit: bloated, self-serving colleges. I’ll be introducing a bill to hold these colleges accountable for debt, lower tuition, support non-college career paths, and save the taxpayers billions.”

Cotton’s comments strike me as purely partisan, at best, and likely incendiary and divisive.

Meanwhile, some on the ultra-progressive side have dismissed this initiative as ‘too little, too late’’, while others on the far right have said, ‘It’s just not fair to those who sacrificed to pay off their student loans; and to those who are more deeply in debt”.

I must confess: I’m not convinced that broad-based blanket cancellation of student loan debt is an optimum solution to the real problem at hand. But, based on current conditions in the world of student loans, it’s probably a necessary step toward creating a new paradigm for educating the future workforce in America.

My personal preference is to look at a problem not just at the surface, but right down to root causes.

[i.e., ‘I don’t like this situation. How can it be fixed?’].

So: What is the real problem, and where do the root causes lie?

I am sympathetic with Sen. Cotton’s sentiment: ‘this plan ignores the true culprit: bloated, self-serving colleges’.

What Sen. Cotton fails to mention is that – beginning in the late 1950’s, and codified by the passage of the federal Vocational Education Act of 1963 — our elected officials created and sustained an environment which enabled an acrimonious socio-economic division between:

- those who go to college to earn a 4-year degree, intending to pursue a ‘white collar’ career;

- those who pursue the training, experience and credentials needed to become a ‘blue-collar’ professional (electrician; plumber; carpenter; auto mechanic; machinist; etc.); and today

- those who opt into a ‘new-collar’ career in a middle-skill job which requires some tech skills, but not a 4-year degree. Some examples include: I-T support; coding; cyber security; and developing web applications.

Passage of The Personal Responsibility and Work Opportunity Reconciliation Act of 1996 marked an expanded view of the value of ‘occupational education’ and the various pathways along career ladders in a wide variety of occupations which would likely lead participants to family wage jobs and careers. Missing from the 1996 legislation was a roadmap to help parents understand, encourage and support their children to pursue their dreams and passions within the framework of economic and financial reality.

Many parents continued to encourage their children to attend a 4-year college to pursue a college diploma in any major, including Art History; Religious Studies; Philosophy; Music Studies; Sociology; Archaeology; English Literature; Film; and myriad other fields, rather than pursue a potentially lucrative vocational education.

College degrees are important and admirable, yet they can result in credentials not valuable or important to employers. From a potential income perspective, some majors are terrible for those who need to borrow – and subsequently repay — loans for tuition and ancillary college expenses.

Some simple interventions which might help transform our currently broken student loan system:

- Mandatory Financial and Economic Education: A critical and logical step to enhance Student Loan Debt Relief is to mandate successful completion of a comprehensive financial and economic education program prior to any student loan borrowings;

- Develop an “income rating system” informed by U.S. Department of Labor projections on salaries and future job openings which would limit the amount of eligible student debt based on major. (See addendum).

- Realistic oversight of private colleges and private lenders: The Financial Crisis of 2007 opened our eyes to private and unregulated ‘shadow bankers’ which originated predatory mortgage loans. There is current evidence that our student loan crisis has been enabled by similar private, lightly regulated lenders which prey on uninformed borrowers, frequently those who are first generation college students and/or those who are enrolled in for-profit colleges.

Dear Senator Cotton: We have identified a few ideas which we think deserve deep and thorough investigation, hopefully leading to appropriate regulatory oversight: a truly honest and valuable use of your time and position. Instead of offering partisan, incendiary and divisive commentary which serves no useful purpose at all, you are invited to use any and all of these ideas to embark on a positive and affirmative journey to make durable and favorable changes to our entire post-secondary system.

Remember the 2020 Recession?

August 11, 2022

I don’t either.

Just because you and I don’t remember the 2020 Recession, that doesn’t mean it didn’t happen.

The official arbiter of recessions — the Bureau of Economic Research — says there was one.

When Donald Trump took office in January 2017, he inherited an economy in its 91st month of economic expansion following the end of the Great Recession in June 2009. That expansion continued into 2020, becoming the longest on record, peaking at 128 months in February 2020.

The National Bureau of Economic Research officially recognized the Recession of 2020 as the shortest on record at just 2 months, with the trough of that recession occurring in April 2020.

One milestone which helps to mark the 2020 recession is the price of oil. During the month of April 2020, the price of a barrel of West Texas Intermediate was absolutely erratic, actually closing Negative at (Minus $37/bbl) on April 20, 2020. [Was gasoline free that day? I don’t recall.]

Back to January 20, 2017, Trump’s Presidential Inauguration Day.

Paul Ryan, a Republican from Wisconsin, was serving as Speaker of the House. Mitch McConnell, a Republican from Kentucky, was the Senate Majority leader.

Ryan was first elected to the House in 1998 at age 28. He developed a reputation as a no-nonsense deficit-hawk fully focused on reducing entitlements and reducing taxes. Ryan had been serving as Speaker of the House since 2015.

The 2017 Tax Cuts and Jobs Act (TCJA) was Paul Ryan’s swan song, eagerly supported by Trump and most congressional Republicans.

Unfortunately, it was exactly the wrong time to enact this complex piece of legislation, primarily because it relied on untested assumptions at a point in time when the U.S. was riding the tail end of the longest economic expansion in history. It created massive increases in our national debt; it favored investment increases in oil and related industries (which to some appeared to be a means to curtail pending increases in oil prices); and exuberant expectations that repatriation of corporate profits parked offshore would be used to create domestic jobs turned into a massive stock buyback across the market.

In early February 2018, Paul Ryan began to reflect on the true consequences of the TCJA. He tweeted, “Julia Ketchum, a secretary at a public high school in Lancaster, Pennsylvania, said she was pleasantly surprised her pay went up $1.50 a week. She didn’t think her pay would go up at all, let alone this soon. That adds up to $78 a year, which she said will more than cover her Costco membership for the year.”

In April 2018, Ryan announced his intention to retire from Congress on January 3, 2019 — the end of his current term — thus ending a 20-year career representing his constituents in Wisconsin — so that he could spend more time with his family.

Left to its own devices, the 2017 TCJA may have created an unchecked economic calamity.

Then came the Covid-19 Pandemic which turned into an unforeseen international societal and economic tragedy – and clearly was the trigger which caused the 2020 recession. Yet, the impacts of Covid didn’t begin to surface until 1st quarter 2020, so there is a 24 month period following the January 2018 introduction of the TCJA which economists are now examining to help create real context around current (mid-2022) economic uncertainties.

Even a neophyte like me can add the 2022 Russian invasion of Ukraine to: (a) the long-term economic damage created by the TCJA; (b) the Covid wild card; and (c) the economic devastation of Trump’s tariffs, particularly on our agriculture sector. When we spread the numbers, we can begin to see an almost perfect recipe created under Trump’s watch sufficient to decimate any economy.

Despite the open hostility and recalcitrance of elected Republicans currently serving in Congress, I must give Joe Biden and the Democrats a 5-Star rating for refusing to capitulate, and for keeping the ball moving forward.

Should We Blame Joe Biden?

June 13, 2022

Stock Prices, Inflation, Recession & Economic Cycles

Economic cycles – also known as business cycles — are a reality, and they can be tracked over time. They generally are predictable, although not in precise time frames. Economic cycles consist of four identifiable phases or stages: (a) Expansion; (b) Peak; (c) Contraction; and (d) Trough.

Every economic cycle includes a period of euphoria and exuberance marked by a sustained period of economic growth; followed by a period of uncertainty and lethargy linked to a period of economic decline.

When Donald Trump took office in January 2017, he inherited an economy in its 91st month of economic expansion following the end of the Great Recession in June 2009. That expansion continued into 2020, becoming the longest period of expansion on record, peaking at 128 months in February 2020.

We know that Donald Trump never fails to speak his mind. During the campaign leading to the 2020 presidential election, Trump proclaimed, “If (Joe Biden) is elected, the stock market will crash!”

[In 2018, Trump said, “When a country (USA) is losing many billions of dollars on trade with virtually every country it does business with, trade wars are good, and easy to win.” In late January 2020, Trump also said, “We have it (coronavirus) totally under control. It’s one person coming in from China. It’s going to be just fine.”]

Facts are facts:

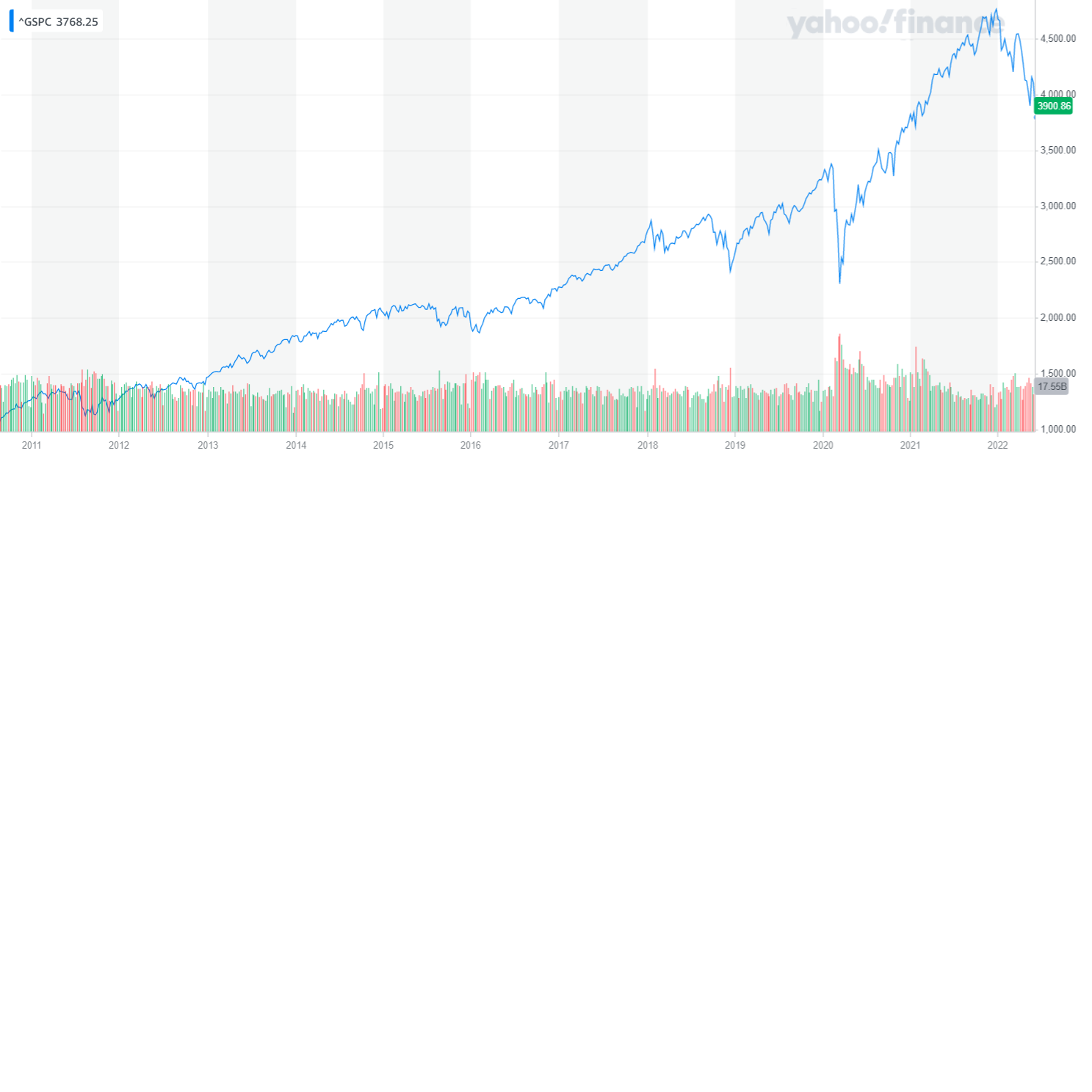

- The S&P 500 fell from 4,766 in late December 2021 to 3,900 today, a 20% loss;

- We’ve seen the price of gasoline hit $5.00 per gallon, up from $3.00 just a year ago;

- Case-Shiller recently reported a 34.8% price increase for housing in the Tampa Bay area (where I currently live) from March 2021 to March 2022;

- The most recent CPI report reflects an annual rate of 8.6 percent through May 2022, the fastest rate in four decades.

What’s really going on?

There are a number of pieces to this puzzle, including:

- The lingering effects of a Pandemic;

- The Russian invasion of Ukraine;

- Aftershocks (direct and indirect) from draconian tariffs enacted beginning in 2018;

- Ongoing ripple effects from the 2017 Tax Cuts and Jobs Act (TCJA); and

- Various supply chain issues, both domestic and international.

But, the root cause of our current intersection of inflation and stock market volatility likely traces back to 2010, when the Fed launched “QE2” – quantitative easing – essentially increasing liquidity in the domestic economy to stimulate economic growth. One of the outcomes from QE is a decrease in bond prices due to falling interest rates, combined with a run-up in stock prices as investors search for yield.

When the Fed announced its QE2 plan in November 2010, 30 year mortgages were at 5%; and the S&P 500 index was 1,200. Over the course of the next few years, rates on 30 year mortgages dropped as low as 3.3%, and the S&P 500 index toward 2,010 (which it reached in September 2014).

Meanwhile, the CPI from 2010 to the end of 2020 remained relatively calm, reflecting the lagging effects of the economic recovery which began in mid-2009.

It is relatively easy to look into the rearview mirror now to observe that the Fed’s response to the impact of Covid on our economy helped to create an environment which fueled the inflation we are facing today. In March 2020, in addition to a promise to inject a $ Trillion into the U.S. banking system, the Fed cut the federal funds rate to a range of 0% to 0.25%.

Those actions of the Fed likely saved our economy from implosion, but also helped to inspire a dramatic run-up in stock prices: The S & P 500 index rose from 3,000 in early March 2020 to reach 4,700 in November 2021. (Stock prices were further affected by massive stock buybacks enabled by the 2017 TCJA).

While it seems convenient for some to blame Joe Biden for high gasoline prices; rapidly rising consumer prices; the stock market ‘meltdown’ — even for supply chain dysfunctions – history tells us there is a rather significant lag between the point when policy actions take place, until begin to see the results from those actions.

The Biden White House has pledged to fight against inflation and has stubbornly refused to blame the Fed for our current economic symptoms.

Although there are plenty of contributing factors, the real truth is over a decade of relying almost entirely on monetary policy to steer the ship brought us to this moment, not 18 months of Democratic control in the White House.

An Economic Genius: Part 2

August 1, 2019

A few weeks ago, I shared some thoughts about our current President and his economic credentials.

Donald John Trump was one of 366 student members of the class of 1968 who was awarded a Bachelor of Science degree in Economics from the Wharton School of Finance and Commerce at the University of Pennsylvania.

Other than his bachelor’s degree and some experience working in the family real estate business, there is no evidence that Mr. Trump has pursued additional education, credentials or capabilities in the field of economics.

Trump’s paucity of bona fides in the world of economic theory and practice has not deterred him from taking an active role in testing new economic theories and concepts.

Below, I introduce a new chapter in my observations on Donald Trump’s economic strategy:

…………………….…………………………………………………………………………………………………………………………………..

July 31, 2019 (Wednesday): Federal Reserve Chairman Powell reluctantly announced a 25bp cut in the federal funds rate, the first rate cut in over a decade (December 2008). In his announcement, Chairman Powell cited, “implications of global developments for the economic outlook as well as muted inflation pressures”. The Fed also referenced an apparent global economic slowdown; uncertainty around U.S.-China trade negotiations; and ‘stubbornly low inflation’.

August 1, 2019 (Thursday): Donald Trump announced (in a series of tweets) that the U.S. would impose a new 10 percent tariff on certain goods from China beginning on September 1, 2019, following the news that trade talks with the China have failed to make sufficient progress.

These new tariffs will apply to the $300 Billion of Chinese goods which had not before faced a tariff. Another $250 Billion of Chinese goods will continue to be tariffed at a 25 percent rate.

This abrupt and unusual move roiled the equity markets, creating a major sell-off.

Since late 2018, the U.S. economy has been showing signs of slowing — bond markets are flaccid; GDP has slowed; new home sales are generally flat; and business investment is anemic, at best.

Virtually every main-stream economist agrees that Trump’s trade war is contributing to the domestic economic malaise, although it’s too early to determine by how much, and if the damage is permanent.

The Fed rate cut on Wednesday was accompanied by a caveat that one purpose was to help create a barrier to prevent Trump’s trade wars from toppling our domestic economy.

Thursday’s surprise announcement by Trump reveals a new, arbitrary, capricious and unilateral decision by the White House which will result in higher taxes to Americans on imports; and further expand uncertainty for businesses which need significant time to manage their supply chains.

The agricultural sector in the U.S. – farms and ancillary industries, suppliers, manufacturers, etc – are already fighting the unexpected impacts of climate and weather on production. Then, they were handed a potential death sentence by a White House which is guided not by strategy and planning, but by impetuous and arbitrary policy changes driven by Trump’s narcissistic compulsions.

If Trump’s Trade War battle plans were conceived within a coordinated environment (i.e. in concert with the Fed and the Congress) perhaps we would be able to see a pathway toward successful outcomes.

Trump is consistent in his bravado that he – and he alone – has the vision, wisdom and solutions to create equilibrium in the trade accounts between the U.S. and China.

According to a BBC analysis from May 2019, “Trump’s decision to take on China could lead to adverse effects for consumers in the US and in China, but also worldwide. An economic showdown between the world’s biggest economies doesn’t look good for anyone.”

Article I of the US Constitution vests the power to set tariffs in Congress, thus Congress has the power to stop this President from continuing his arbitrary and impetuous trade war. The question remains: Will elected officials in Congress wake up, do their job and use that power, or will they continue to abdicate legislative responsibilities to this President?

An Economic Genius: Part One

July 9, 2019

Donald John Trump was one of 366 student members of the class of 1968 who was awarded a Bachelor of Science degree in Economics from the Wharton School of Finance and Commerce at Pennsylvania State University (Penn State).

Other than his bachelor’s degree and some experience working in the family real estate business, there is no evidence that Mr. Trump has pursued additional education, credentials or capabilities in the field of economics.

Trump’s paucity of bona fides in the world of economic theory and practice has not deterred him from taking an active role in testing new economic concepts.

From an economic perspective, the presidency of Donald Trump will likely be remembered primarily for his America First posture, which has influenced immigration, tariff and tax policies.

Immigration: Trump administration policy decisions focused on immigration have dramatically hurt domestic agriculture, food processing, hospitality, tourism and other low-wage, entry-level service occupations.

Tariffs: Tariffs imposed on imported goods and materials are nothing more than a tax paid by the end user, in many cases, the American consumer.

Tariffs can be effectively used as a component of a strategic long-term plan to reposition the competitive position of American manufacturers on the world stage.

There is no known evidence that tariffs have ever brought any long-term value-added when arbitrarily and capriciously applied.

Trump administration subjective tariffs on imported steel and aluminum (justified as a means to “protect our country and our workers”) have proven to be a financial burden on several high-wage value-added U.S. industries, including: Automotive; Aerospace; Construction; and Manufacturing.

Tax Cuts: The signing of the Tax Cuts and Jobs Act in December 2017 was lauded as landmark legislation which would: (a) lower taxes on businesses and individuals; (b) stimulate higher wages and more jobs; and (c) result in a larger and more dynamic economy as a result of dramatically increased domestic business investment in plant and equipment.

Almost two years after the passage of TCJA, it seems clear that some near-term economic stimulation was achieved, but the long-term impact on gross domestic product (GDP) will be modest, if at all. The impact will be smaller on gross national product (GNP) than on GDP because the law generated net capital inflows from abroad that must be repaid in the future.

The expectation touted by elected officials in their frenzy to pass the TCJA envisioned some $4 Trillion being repatriated, generating new and potent investment and jobs in the U.S.

Most recent estimates reflect $3 Trillion (or more) in profits that U.S. companies have left parked overseas, with about $465 Billion in “repatriated” cash returning to the U.S. to enjoy a tax rate of 15.5% (vs. the 35% prior tax rate) on profits returned to the U.S. from overseas.

A good outcome? Sure, in the short term. Capital investments? Plant and equipment? Not so much. There is virtually no evidence that any of the repatriated cash was invested in job creation. It was invested in executive bonuses; stock buy-backs; debt repayments; and some dividend enhancements.

Please stay tuned, there is more to come…..

Mueller Report

May 29, 2019

Several of my friends have wondered: What part of “… this report does not conclude that the President committed a crime, it also does not exonerate him” supports the “No Collusion, No Obstruction” response from the Trump White House.

My theory is based on a variety of academic studies over the past 2 decades which have determined that an ‘average American adult’ reads at (or about) the eighth grade level.

The reading skills of American adults are significantly lower than those of adults in most other developed countries, according to a study by the Organization for Economic Cooperation and Development based on a sample of 160,000 people from two dozen developed nations.

The Mueller Report is an academic treatise written at a level which clearly exceeds the abilities of most American adults to engage; read; analyze; and conclude.

The ability to read fluently, critically and for understanding— to be able to learn from text— may be the most important foundational skill for U.S. adult citizens’ health, well-being, and social and economic advancement.

Critical reading skills are the gateway to lifelong learning, education, and training.

The internet and social networking currently operate through the written word, thus reading literacy provides access to an infinite and readily accessible library of the world’s knowledge, as well as the ability to communicate with friends, family, and employers.

The digital revolution provided access to information which is the foundation for an informed society — except for those adults who continue to struggle to read and/or comprehend.

We have a crisis in America. The Mueller Report is written at a level which exceeds the skills of the majority of Americans — including many of those currently serving in Congress — to understand, analyze and arrive at critically informed conclusions.

The Pew Research Center recently reported that adults with a high school degree (or less) represent the majority (37%) of U.S. adults who report not reading books in any format in the past year.

I have to wonder – and I hope you will join me — How many of these 37% of adults who don’t read books (and perhaps don’t read critically?) are members of the Trump Base?