Federal Debt Ceiling Observations

May 11, 2023

Hanging their hats on false equivalence

The underlying logic Speaker Kevin McCarthy and his crew lean on in their arguments relative to the federal debt ceiling rely on false equivalencies.

The gist of their message seems to be, “Just as families and businesses balance their checkbooks every month, we believe the federal government needs to make balancing the nation’s checkbook a top priority. Raising the debt ceiling is a short-term solution to a long- term problem. Before we consider raising the debt ceiling, our federal government needs to focus on reducing spending and living within its means to ensure a healthy economy for future generations”.

Sounds pretty good, right?

Yet, that explanation illuminates one of the greatest obstacles we face as a nation: A void of economic and financial understanding among most American adults.

The ‘checkbook’ is the equivalent of an annual budget. Current revenues flow in, and current expenses flow out. If revenues exceed expenses, there is a surplus. When revenues exactly equal expenses, it is ‘break even’. When expenses exceed revenues, there is a current-year deficit.

Staying with the household theme, the federal debt is most equivalent to a home mortgage, and the balance due is an accumulation of debt over time. Remember that new roof? That new kitchen? That fabulous backyard pool? Those were capital expenses, incurred in one year, but with an expected useful life of 10, 15, even 30 years. You add these expenses to the mortgage so that they get paid off over time.

As a retired professional in the field of finance and economics, when I hear Speaker McCarthy or members of his crew attempting to equate current spending to our overall aggregate debt obligations, I cringe.

Some rather simple adjustments to our tax code, including elimination of the carried interest loophole and raising the top corporate rate from 21% to 28% would make huge revenue contributions to balancing the annual (current FY) federal budget.

And, why is it that low- and moderate-income wage earners are required to make contributions to Social Security on every dollar of their earnings up to the current wage cap [a.k.a. ‘the contribution and benefit base’] of $160,200, yet those who are blessed to earn in excess of that amount are exempt from contributions to Social Security on earnings above that amount?

The wage cap on Medicare contributions was eliminated in the 1990’s, so even higher-income wage earners are required to make the 1.45% contribution to the Medicare tax with no limit on earnings.

We clearly have a revenue gap. Why does the cap on social security earnings continue to this day? And, those who claim their income not as ‘wages’ but as ‘carried interest’ not only receive beneficial income tax treatment, they also are exempt from FICA contributions. What a racket!

Federally guaranteed obligations are debt securities issued by the U.S. government, currently considered risk-free because they are backed by the full faith and credit of the federal government. When the Treasury sells these securities, they help to finance the federal debt outstanding at that time.

Allowing the government to default as an outcome from a false debate linking current revenues and spending to our long-term debt obligations would be a preventable tragedy of immense proportions.

Minority Leader Hakeem Jeffries (if you are listening): I implore you to be bold and to tear apart Speaker McCarthy’s logic map, and to take this opportunity to focus in on one of the greatest obstacles we face as a nation: A void of economic and financial understanding among most American adults. Until the American people awake from their deprivation of economic and financial principles, they will continue to be vulnerable to Alternative Facts such as those presented by Speaker McCarthy and his crew.

The Big Lebowski must have learned of McCarthy’s foolish and destructive crusade to equate and combine the federal debt ceiling with the current (2024) federal budget when he so eloquently said, “This will not stand, you know. This aggression will not stand, man”.

Remember the 2020 Recession?

August 11, 2022

I don’t either.

Just because you and I don’t remember the 2020 Recession, that doesn’t mean it didn’t happen.

The official arbiter of recessions — the Bureau of Economic Research — says there was one.

When Donald Trump took office in January 2017, he inherited an economy in its 91st month of economic expansion following the end of the Great Recession in June 2009. That expansion continued into 2020, becoming the longest on record, peaking at 128 months in February 2020.

The National Bureau of Economic Research officially recognized the Recession of 2020 as the shortest on record at just 2 months, with the trough of that recession occurring in April 2020.

One milestone which helps to mark the 2020 recession is the price of oil. During the month of April 2020, the price of a barrel of West Texas Intermediate was absolutely erratic, actually closing Negative at (Minus $37/bbl) on April 20, 2020. [Was gasoline free that day? I don’t recall.]

Back to January 20, 2017, Trump’s Presidential Inauguration Day.

Paul Ryan, a Republican from Wisconsin, was serving as Speaker of the House. Mitch McConnell, a Republican from Kentucky, was the Senate Majority leader.

Ryan was first elected to the House in 1998 at age 28. He developed a reputation as a no-nonsense deficit-hawk fully focused on reducing entitlements and reducing taxes. Ryan had been serving as Speaker of the House since 2015.

The 2017 Tax Cuts and Jobs Act (TCJA) was Paul Ryan’s swan song, eagerly supported by Trump and most congressional Republicans.

Unfortunately, it was exactly the wrong time to enact this complex piece of legislation, primarily because it relied on untested assumptions at a point in time when the U.S. was riding the tail end of the longest economic expansion in history. It created massive increases in our national debt; it favored investment increases in oil and related industries (which to some appeared to be a means to curtail pending increases in oil prices); and exuberant expectations that repatriation of corporate profits parked offshore would be used to create domestic jobs turned into a massive stock buyback across the market.

In early February 2018, Paul Ryan began to reflect on the true consequences of the TCJA. He tweeted, “Julia Ketchum, a secretary at a public high school in Lancaster, Pennsylvania, said she was pleasantly surprised her pay went up $1.50 a week. She didn’t think her pay would go up at all, let alone this soon. That adds up to $78 a year, which she said will more than cover her Costco membership for the year.”

In April 2018, Ryan announced his intention to retire from Congress on January 3, 2019 — the end of his current term — thus ending a 20-year career representing his constituents in Wisconsin — so that he could spend more time with his family.

Left to its own devices, the 2017 TCJA may have created an unchecked economic calamity.

Then came the Covid-19 Pandemic which turned into an unforeseen international societal and economic tragedy – and clearly was the trigger which caused the 2020 recession. Yet, the impacts of Covid didn’t begin to surface until 1st quarter 2020, so there is a 24 month period following the January 2018 introduction of the TCJA which economists are now examining to help create real context around current (mid-2022) economic uncertainties.

Even a neophyte like me can add the 2022 Russian invasion of Ukraine to: (a) the long-term economic damage created by the TCJA; (b) the Covid wild card; and (c) the economic devastation of Trump’s tariffs, particularly on our agriculture sector. When we spread the numbers, we can begin to see an almost perfect recipe created under Trump’s watch sufficient to decimate any economy.

Despite the open hostility and recalcitrance of elected Republicans currently serving in Congress, I must give Joe Biden and the Democrats a 5-Star rating for refusing to capitulate, and for keeping the ball moving forward.

Tax Exempt for Religious Purposes

June 15, 2022

This property – a 50-unit vacation destination – was acquired by the Church of Scientology FLAG Service Organization in 1996. Although it is currently assessed for $2.3 Million, it has been off the tax rolls since 2013. That’s right. This 50-unit waterfront motel is tax exempt for religious purposes.

The property is now gated and clearly not accessible to the public, yet it appears to be well-maintained and suitable for its intended use as temporary housing for travelers.

In a post from November 2020, Mike Rinder looked deeply into the concept of awarding tax exemption to the Church of Scientology (Scientology’s Tax Exemption (mikerindersblog.org)

I am resident, voter, property owner and taxpayer in Clearwater, FL where the Church of Scientology has directly and indirectly acquired hundreds of properties, taking many off the tax rolls thus shifting the tax burden to others.

I don’t wish to debate the validity of the religious exemption Scientology won from the IRS, yet I do want to debate the practice of hiring and using an army of lawyers to fight property assessors who attempt to determine that some of the properties owned by Scientology are not used for religious or charitable purposes, and thus not eligible for property tax exemptions.

I also question many of the activities of Scientology which seem to confer ‘excess benefits’ to Chairman Miscavige and others who occupy senior positions in the Organization.

Having received tax exemption from the IRS as a religious organization, the Church of Scientology and its many affiliates are also exempt from filing an annual Form 990 “Information Return” with the IRS:

‘They are encouraged to file, but not required to file.’

The 990 provides a treasure trove of information, including executive compensation, benefits, governance, etc.

If I was a gangster posing as a religious leader, I would want to be exempt from any public disclosure, including the requirement to file a 990.

If I was an honest, fair, selfless religious leader I would hope to be fairly compensated for my education, wisdom and service so that I had adequate shelter, nutrition and safety for me and my household, but I wouldn’t object to disclosing the financial affairs of my organization, which would include disclosure of my personal compensation and benefits.

This goes well beyond Scientology as there are more than a few Exempt Religious Organizations which opt into the nondisclosure arena.

Despite that loophole, a rather large number of religious organizations which have received tax exemption from the IRS continue to file their 990 forms every year.

This seems to be another serious, dangerous and egregious loophole in our Federal Tax Code that needs to be addressed.

We, The People, ought to know what is going on behind the curtain, particularly because we are left paying the piper when those few tax-exempt organizations every year stray from the garden path.

Should We Blame Joe Biden?

June 13, 2022

Stock Prices, Inflation, Recession & Economic Cycles

Economic cycles – also known as business cycles — are a reality, and they can be tracked over time. They generally are predictable, although not in precise time frames. Economic cycles consist of four identifiable phases or stages: (a) Expansion; (b) Peak; (c) Contraction; and (d) Trough.

Every economic cycle includes a period of euphoria and exuberance marked by a sustained period of economic growth; followed by a period of uncertainty and lethargy linked to a period of economic decline.

When Donald Trump took office in January 2017, he inherited an economy in its 91st month of economic expansion following the end of the Great Recession in June 2009. That expansion continued into 2020, becoming the longest period of expansion on record, peaking at 128 months in February 2020.

We know that Donald Trump never fails to speak his mind. During the campaign leading to the 2020 presidential election, Trump proclaimed, “If (Joe Biden) is elected, the stock market will crash!”

[In 2018, Trump said, “When a country (USA) is losing many billions of dollars on trade with virtually every country it does business with, trade wars are good, and easy to win.” In late January 2020, Trump also said, “We have it (coronavirus) totally under control. It’s one person coming in from China. It’s going to be just fine.”]

Facts are facts:

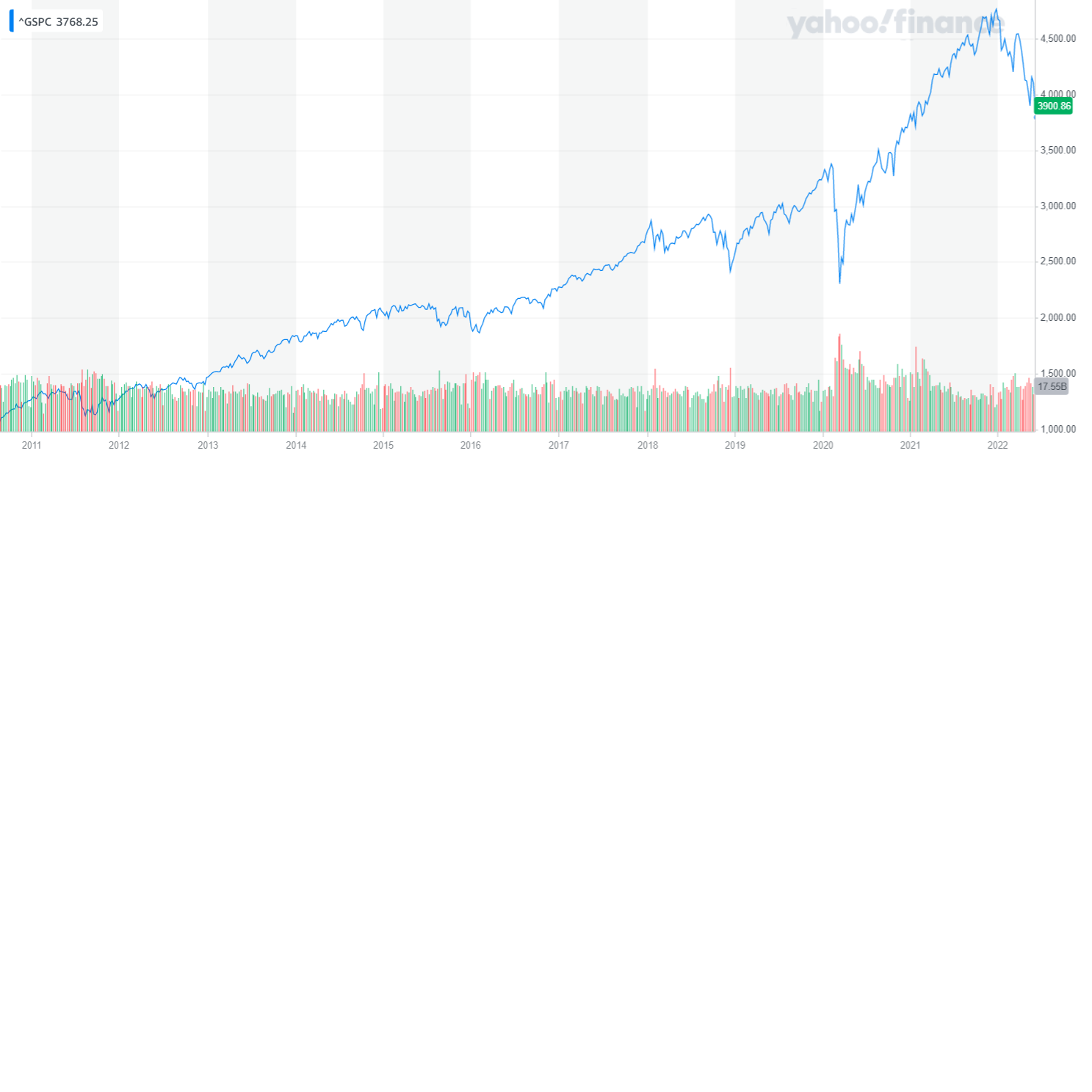

- The S&P 500 fell from 4,766 in late December 2021 to 3,900 today, a 20% loss;

- We’ve seen the price of gasoline hit $5.00 per gallon, up from $3.00 just a year ago;

- Case-Shiller recently reported a 34.8% price increase for housing in the Tampa Bay area (where I currently live) from March 2021 to March 2022;

- The most recent CPI report reflects an annual rate of 8.6 percent through May 2022, the fastest rate in four decades.

What’s really going on?

There are a number of pieces to this puzzle, including:

- The lingering effects of a Pandemic;

- The Russian invasion of Ukraine;

- Aftershocks (direct and indirect) from draconian tariffs enacted beginning in 2018;

- Ongoing ripple effects from the 2017 Tax Cuts and Jobs Act (TCJA); and

- Various supply chain issues, both domestic and international.

But, the root cause of our current intersection of inflation and stock market volatility likely traces back to 2010, when the Fed launched “QE2” – quantitative easing – essentially increasing liquidity in the domestic economy to stimulate economic growth. One of the outcomes from QE is a decrease in bond prices due to falling interest rates, combined with a run-up in stock prices as investors search for yield.

When the Fed announced its QE2 plan in November 2010, 30 year mortgages were at 5%; and the S&P 500 index was 1,200. Over the course of the next few years, rates on 30 year mortgages dropped as low as 3.3%, and the S&P 500 index toward 2,010 (which it reached in September 2014).

Meanwhile, the CPI from 2010 to the end of 2020 remained relatively calm, reflecting the lagging effects of the economic recovery which began in mid-2009.

It is relatively easy to look into the rearview mirror now to observe that the Fed’s response to the impact of Covid on our economy helped to create an environment which fueled the inflation we are facing today. In March 2020, in addition to a promise to inject a $ Trillion into the U.S. banking system, the Fed cut the federal funds rate to a range of 0% to 0.25%.

Those actions of the Fed likely saved our economy from implosion, but also helped to inspire a dramatic run-up in stock prices: The S & P 500 index rose from 3,000 in early March 2020 to reach 4,700 in November 2021. (Stock prices were further affected by massive stock buybacks enabled by the 2017 TCJA).

While it seems convenient for some to blame Joe Biden for high gasoline prices; rapidly rising consumer prices; the stock market ‘meltdown’ — even for supply chain dysfunctions – history tells us there is a rather significant lag between the point when policy actions take place, until begin to see the results from those actions.

The Biden White House has pledged to fight against inflation and has stubbornly refused to blame the Fed for our current economic symptoms.

Although there are plenty of contributing factors, the real truth is over a decade of relying almost entirely on monetary policy to steer the ship brought us to this moment, not 18 months of Democratic control in the White House.

An Economic Genius: Part One

July 9, 2019

Donald John Trump was one of 366 student members of the class of 1968 who was awarded a Bachelor of Science degree in Economics from the Wharton School of Finance and Commerce at Pennsylvania State University (Penn State).

Other than his bachelor’s degree and some experience working in the family real estate business, there is no evidence that Mr. Trump has pursued additional education, credentials or capabilities in the field of economics.

Trump’s paucity of bona fides in the world of economic theory and practice has not deterred him from taking an active role in testing new economic concepts.

From an economic perspective, the presidency of Donald Trump will likely be remembered primarily for his America First posture, which has influenced immigration, tariff and tax policies.

Immigration: Trump administration policy decisions focused on immigration have dramatically hurt domestic agriculture, food processing, hospitality, tourism and other low-wage, entry-level service occupations.

Tariffs: Tariffs imposed on imported goods and materials are nothing more than a tax paid by the end user, in many cases, the American consumer.

Tariffs can be effectively used as a component of a strategic long-term plan to reposition the competitive position of American manufacturers on the world stage.

There is no known evidence that tariffs have ever brought any long-term value-added when arbitrarily and capriciously applied.

Trump administration subjective tariffs on imported steel and aluminum (justified as a means to “protect our country and our workers”) have proven to be a financial burden on several high-wage value-added U.S. industries, including: Automotive; Aerospace; Construction; and Manufacturing.

Tax Cuts: The signing of the Tax Cuts and Jobs Act in December 2017 was lauded as landmark legislation which would: (a) lower taxes on businesses and individuals; (b) stimulate higher wages and more jobs; and (c) result in a larger and more dynamic economy as a result of dramatically increased domestic business investment in plant and equipment.

Almost two years after the passage of TCJA, it seems clear that some near-term economic stimulation was achieved, but the long-term impact on gross domestic product (GDP) will be modest, if at all. The impact will be smaller on gross national product (GNP) than on GDP because the law generated net capital inflows from abroad that must be repaid in the future.

The expectation touted by elected officials in their frenzy to pass the TCJA envisioned some $4 Trillion being repatriated, generating new and potent investment and jobs in the U.S.

Most recent estimates reflect $3 Trillion (or more) in profits that U.S. companies have left parked overseas, with about $465 Billion in “repatriated” cash returning to the U.S. to enjoy a tax rate of 15.5% (vs. the 35% prior tax rate) on profits returned to the U.S. from overseas.

A good outcome? Sure, in the short term. Capital investments? Plant and equipment? Not so much. There is virtually no evidence that any of the repatriated cash was invested in job creation. It was invested in executive bonuses; stock buy-backs; debt repayments; and some dividend enhancements.

Please stay tuned, there is more to come…..

The Sport of Tax Avoidance

May 11, 2019

Let’s be clear: the terms ‘tax evasion’ and ‘tax avoidance’ are often used interchangeably. However, only those activities which occur in a tax avoidance scheme are considered lawful.

Plenty of reliable media sources have carefully examined and reported on the awful legacy of Donald Trump’s multiple bankruptcies on a myriad of small businesses: architects, carpet suppliers, lighting and electrical distributors, even custom cabinet-makers.

A recent expose published by The New York Times focused on Trump’s taxes and revealed a previously unexposed nuance: many of his unpaid bills were essentially ‘double counted’ through the magic of accrual accounting. Thus, Trump and his Organization underpaid many vendors, while concurrently creating a paper loss for Trump which translated into a ‘tax loss carryforward’ good to shield future profits from future taxation.

If people had been able to look at this bad behavior as a base line, and project it forward, they might have been able to see how much damage The Donald has already done to families and communities in the U.S.

Following his inauguration in January 2017, Trump’s operating principles haven’t changed at all.

A direct result of the introduction of Trump operating principles into the Executive Office has become an oblique assault on moderate and small family-owned businesses across the U.S. — in the manufacturing sector; in retail; agriculture; mining; ranching; hospitality; media; transportation; entertainment; food; construction; business services; technology; and more.

The foundation of success epitomized in the American Dream is entrepreneurial — hard work, focus and sacrifice oriented to a long term view.

The minority of small business operators who operate like Trump — those who operate at the margins and take advantage of honest business people who operate on the platform of honesty and honor — get put out of business quickly.

Tax avoidance – using any and every loophole to avoid paying taxes – is legal, even when some of the activities involved may be considered by some to be morally repugnant.

Somehow, Trump has been able to use his unique combination of charisma and showmanship to fool a rather sizeable segment of American adults into believing his shtick.

How very sad…

More on: Tax Cuts & Jobs Act

April 16, 2019

Paul Ryan retired from Congress in January 2019 after 20 years of service culminating in his 3+ years of service as Speaker of the House.

Ryan was the chief cheerleader for the Tax Cuts and Jobs Act, and he left D.C. touting it as the greatest accomplishment of his political career.

Ryan repeatedly exclaimed how this new legislation (TCJA) would unleash unprecedented U.S. economic prosperity, by providing:

- Tax relief for middle-income families;

- Simplification of the tax code for individuals;

- Economic growth; and

- Repatriation of $3+ Trillion of profits U.S. companies have parked overseas would generate more investment and jobs in the U.S.

16 months after passage of the TCJA, it should be crystal clear that:

- Almost none of the tax cut benefits have reached the low- and middle income Americans who were promised tax relief;

- The TCJA legislation is some 1,097 pages itself, and it states very clearly that it is an Amendment to (the existing) Internal Revenue Code of 1986 (not a simplification);

- Economic Growth? The jury is still out on this one, but there seems to be no evidence of growth above or beyond the existing growth trend line which began in mid-2009;

- American companies have returned some (+/- $500 Billion) of their profits held overseas as a result of the tax holiday which was part of TCJA. Much of that money was used for stock buy-backs and debt reduction.

In fact, 16 months following the passage of the TCJA, U.S. companies are still waiting for final guidance from the Treasury Department on many of the final rules relative to repatriation.

And, despite continued U.S. economic growth and record corporate profits, a record 60 Fortune 500 companies avoided paying any federal income tax in 2018.

Federal tax revenues have declined during a period of economic expansion and our government spending has increased, thus the verifiable result from Paul Ryan’s signature accomplishment – the TCJA — is an increase in our federal deficit, an extra-special gift to our children and grandchildren.

The Treasury Department announced in March 2019 that the deficit for the first four months of the 2019 budget year (which began Oct. 1, 2018) totaled $310.3 Billion, up from a deficit of $175.7 Billion in the same period the year prior.

The Congressional Budget Office is projecting that the annual federal deficit between revenues and expenses will hit $897 Billion in fiscal year 2019, up 15.1 percent from the $779 Billion deficit recorded in FY 2018.

The end result: Our total federal debt will reach $22 Trillion this year – about 105% of GDP.

Why is that important? A comprehensive study by the World Bank examined economic data from 100 developing and developed economies spanning a time period from 1980 to 2008, concluding that a public debt/GDP above 77% begins to create a drag on economic growth.

The World Bank analysis concluded that for each additional percentage point of debt above the 77% threshold costs 0.017 percentage points of annual real growth.

If the World Bank study is correct, we are currently missing about 0.5% of our economic growth potential due to misguided public policy decisions, in addition to the future burden of repaying federal debt which was incurred unnecessarily.

Paul Ryan achieved his personal goal of shepherding record tax reform through Congress resulting in the passage of TCJA.

Although his personal goal was achieved at the expense of American society, Paul Ryan clearly is a winner. So, please join me in sending a note of thanks and congratulations to Paul Ryan. He left us a legacy.

The Amazon Conundrum

March 5, 2019

While New Yorkers continue to debate the loss of Amazon from a site in Queens, the discussion seems to have lost sight of what Amazon contributes to the long-term well-being of our society.

Amazon is not a friend to America, has contributed very little if anything to our overall economy. The stock is currently grossly overvalued with a P/E ratio in excess of 80x.

Jeff Bezos, the founder of Amazon, has an estimated net worth of $165 Billion, primarily as a result of a business model which has dramatically changed the U.S. retail sector.

Most egregious? Amazon paper earnings for 2018 are $11.2 Billion, and early reports indicate that they will pay $0 in federal income taxes on these earnings.

(Amazon reported $5.6 Billion in U.S. profits in 2017 and paid $0 last year.)

Amazon creates jobs? True. Good jobs? False.

Economic scholars generally agree that a ‘living wage’ in the NY Metro area for an adult with one child is $31/hour, with 2 children $41/hour.

Amazon announced in early October 2018 that it would raise the minimum wage to $15 an hour for its U.S. employees.

Meanwhile, much like Walmart, Amazon has created a business model which effectively eliminates competition and destroys small business.

The hot topic today is the talk of ‘Democratic Socialism’ being portrayed by some pundits as a death threat to American democracy.

The real threat to American democracy is the proliferation and exponential growth of a few family-controlled and vertically-integrated oligarchies which are capable of re-creating the Feudal System which characterized medieval Europe during the Middle Ages.

“Those who fail to learn from the lessons of history are bound to repeat the outrage of history.”

National Emergency

February 13, 2019

Yes, we are facing a national emergency, and it’s not along our southern border.

Our real national emergency is our National Debt.

Let’s first agree that when the U.S. federal government runs a deficit, or spends more than it receives in tax revenue, the U.S. Treasury Department borrows money to make up the difference.

Next, let’s agree that our national debt is the amount of money the federal government has borrowed through various means, including: (1) by issuing bills, notes and bonds which are bought by investors (domestic and foreign), including the public, the Federal Reserve and foreign governments; (2) through intra-governmental debt, essentially money borrowed from trust funds used to pay for programs like Social Security and Medicare.

The great majority of economists and economic and fiscal analysts tend to agree that the significance of national debt is best measured by comparing the debt with the federal government’s ability to pay it off using the debt-to-GDP ratio, simply by dividing a nation’s debt by its gross domestic product.

Various sources have estimated that a healthy debt-to-GDP ratio is in the 40% to 60% range. A longitudinal study conducted by World Bank economists published in 2010 estimated that in highly developed countries, 77% was a ‘tipping point’ where productivity and potential economic growth was constrained by adding additional debt without addition of incremental revenue. (In emerging economies, they estimate that 64% is the tipping point.) In either case, potential for default begins to increase once the tipping point has been breached, thus putting upward pressure on borrowing costs.

The first instance when U.S. debt-to-GDP ratio exceeded 77% was toward the end of World War II. In the post-war years, our national debt shrank in comparison to the booming post-war economy, and the debt-to-GDP ratio fell as low as 24 percent in 1974.

Recession and rising interest rates during the Carter administration put upward pressure on the debt-to-GDP ratio, and once the tax cuts enacted during Reagan’s first term combined with increased spending on both defense and social programs, the debt-to-GDP ratio reached 50 % in July 1989.

Economic growth in the ‘90s, combined with tax increases under both Presidents George H.W. Bush and Bill Clinton helped keep the debt load in line, and by the end of December 2000, our national debt was about 55% of GDP.

Following the terrorist attacks on 9/11/2001, U.S. military spending spiked, yet tax cuts enacted in 2001 and 2003 during the George W. Bush administration combined with a mild recession in 2001 and the Great Recession beginning in 2007 caused significant decreases in tax revenues. By the time Barack Obama took office in January 2009, the debt-to- GDP-ratio reached 75%.

Deficit spending is one of the key tools available to stimulate economic recovery, and by the time of Obama’s 2nd inauguration in January 2013, the U.S. debt had grown to $16 Trillion – a debt-to-GDP ratio of 101%. By that time, it was clear that the economic stimulus of deficit spending had worked, evidenced by an expanding U.S. economy; signs of ending the wars in Afghanistan and Iraq; resurgence of the U.S. stock market; continued job growth; and other positive economic indicators.

All of these positive signs at the beginning of 2013 pointed to the need to rein in government spending and to strategically increase revenues (i.e. raise taxes).

Yet, the Congress has stubbornly refused to deal with the reality that our U.S. debt-to-GDP ratio has remained above 100 percent since 2013.

In early 2018, an analysis by the nonpartisan Committee for a Responsible Federal Budget concluded that the Tax Cuts and Jobs Act signed into law in late 2017 will push the U.S. national debt to $33 Trillion — 113 % of GDP — by 2028, a ratio not seen since immediately after World War II.

The Tax Cuts and Jobs Act is a sham (and a scam) which created a situation exactly opposite of what responsible elected officials should have supported. The sooner it is amended, repaired or repealed, the sooner the American people will be transitioned into a less dangerous and more stable and sustainable economic environment.

Economic and Fiscal Policy

February 12, 2019

Our current POTUS rarely stands still long enough for anyone to really examine how his positions and policies impact us in the present, or potentially in the future.

Here are a couple of observations which I managed to glean from rapidly moving targets:

Fiscal Policy: Failure

By late 2017, the U.S. economy had enjoyed over 8 years of economic expansion (since June 2009), leading virtually all economists to conclude we were moving toward the end of an economic expansion cycle. Most experts agree that the government should constrain both borrowing and spending during an expansion phase, concurrently decreasing government debt.

When the expansion phase of a business cycle comes to an end, and the economy begins to sputter – and ultimately to contract – a government with reduced debt will have the capacity to spend more and tax less, helping to support the softening economy return to equilibrium faster and smoother.

The much-touted Tax Cuts and Jobs Act enacted at the end of 2017 introduced a $1.5 Trillion tax cut, sold as a source of economic stimulus when it was least needed.

In times of economic expansion, the government is on notice to reduce its deficit.

On February 12, 2019, the national debt passed a new milestone, topping $22 Trillion for the first time. According to the U.S. Treasury Department, total outstanding public debt hit $22.01 Trillion, up from the $19.95 Trillion when President Donald Trump took office on Jan. 20, 2017. This is mighty dangerous stuff, folks.

Trade Policy: Failure

Tariffs are a tax on consumption, paid by end users.

Over several decades, the U.S. developed a dependence on manufactured goods from China. In turn, U.S. exports to China – predominantly agricultural and unfinished goods – enjoyed strong growth over time.

President Trump abruptly started a trade war with China, imposing tariffs on goods imported into the U.S. beginning in July 2018.

China quickly retaliated, raising tariffs on American goods imported into China, resulting in significant shifts by China to alternative sources.

Winners? Brazil; Russia; Germany; Japan.

Losers? American agricultural producers in Iowa, Nebraska, Indiana, Missouri, Ohio, South Dakota, North Dakota, and Kansas; some American manufacturers; and American consumers overall.

It was once said, “When a country (USA) is losing many billions of dollars on trade with virtually every country it does business with, trade wars are good, and easy to win.”

The evidence seems to emphatically refute that position.